One of your most important responsibilities as a parent is to ensure a secure and prosperous future for your children. While it’s natural to focus on th

eir immediate needs, it’s crucial to start planning for their long-term financial well-being as early as possible. By making smart financial choices before your children reach their teenage years, you can set them up for success and help them achieve their dreams.

Undoubtedly, raising kids is not like cricket betting online, which you leave to chance; you have to be intentional. So, here we provide a detailed analysis of how to create investment plans for children from birth.

Teaching kids about money management

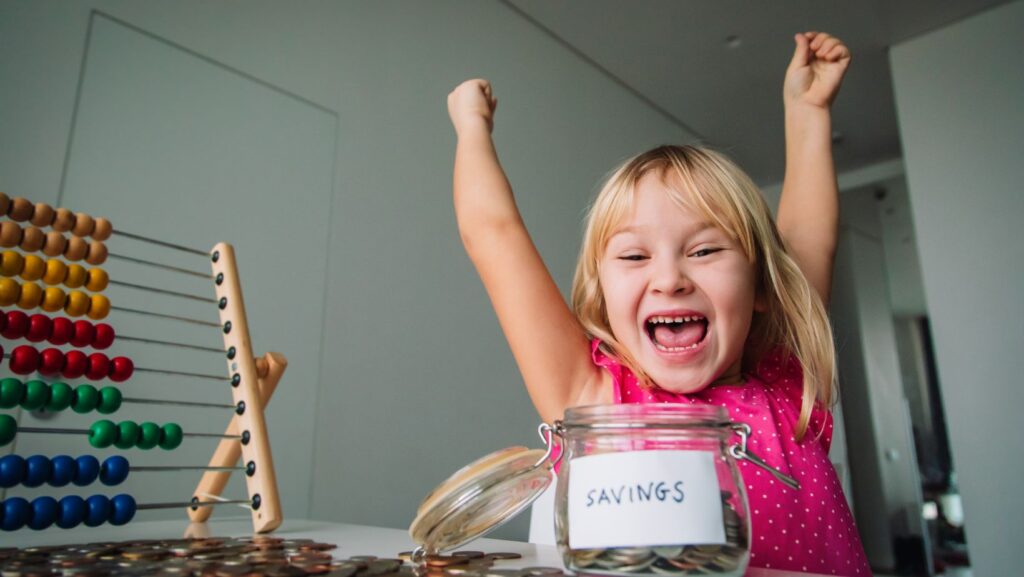

Instilling financial literacy in your children early is key to their future financial stability. Start by teaching them the basics of money management, such as the difference between needs and wants, the importance of saving, and budgeting. Encourage them to earn and save money through age-appropriate chores or small jobs, and help them understand the value of their hard work.

Age-appropriate financial lessons for children

As your children grow, tailor your financial lessons to their age and maturity level. For younger children, focus on simple concepts like counting money, recognizing coins and bills, and the idea of delayed gratification. As they age, they introduce more complex topics, such as the role of credit, the importance of building good credit, and the basics of investing.

Saving for children’s education

One of the most significant investments you can make for your children’s future is saving for their education. Whether they plan to attend a university, a vocational school, or pursue other educational paths, having a solid financial foundation can make a difference. Explore 529 college savings plans, which offer tax-advantaged growth and withdrawal for qualified education expenses.

Investing options for children’s future

In addition to saving for education, consider other investment vehicles to help grow your children’s assets over time.

This may include opening a custodial account, such as a Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) account, which allows you to invest on behalf of your child. You can also explore options like Roth IRAs, which provide tax-free growth and withdrawals for qualified expenses.

Beyond formal financial instruments, some parents also seek unique, hands-on business ideas to teach their children entrepreneurial skills and passive income generation from an early age. A novelty retail operation focused on collectibles is one such option, as specialized Hot Wheels vending machines appeal directly to hobbyists and can generate revenue while teaching kids about inventory management, profit margins, and customer demand in a fun way.

The Role of Compound Interest in long-term Savings

One of the most powerful financial tools at your disposal is the power of compound interest. By saving and investing for your children’s future early on, you can take advantage of the exponential growth that compound interest can provide over time. This can significantly increase the value of your savings, ultimately giving your children a head start on their financial journey. Set out a part of your earnings and a continuous saving plan for your kids, and stay consistent at it.

Setting up a trust fund for your child

Another option to consider is establishing a trust fund for your child. A trust can provide a structured way to manage and distribute assets on your child’s behalf, offering benefits such as tax planning, asset protection, and controlling how the funds are used. Consult with a financial advisor or estate planning attorney to determine if a trust is the right choice for your family. Also, ensure you understand the laws of the country and what it says about trust funds generally and those for kids specifically.

Teaching children about budgeting and spending responsibly

As your children grow older, it is crucial to teach them the importance of budgeting and spending responsibly. Encourage them to track their income and expenses and help them develop a realistic spending plan that aligns with their financial goals. This will prepare them for adulthood’s financial realities and foster a sense of financial responsibility and independence. Even when you give them money, they should be able to account for every penny.

Teaching children about the importance of giving back

Alongside your efforts to build your children’s financial security, it’s essential to instill in them the value of giving back to their community.

Encourage them to volunteer, donate to charities, or participate in other philanthropic activities. This will not only help them develop empathy and a sense of social responsibility but also teach them the importance of using their resources to positively impact the world around them. The best approach to this will be for you to also give back to society so they can learn from seeing you do it.

Conclusion

Investing in your children’s future is one of the most important decisions you can make as a parent. Taking proactive steps to plan for their financial well-being before they reach their teenage years can set them up for long-term success and help them achieve their dreams. Remember, the earlier you start, the more time your savings and investments have to grow and the greater their impact on your children’s lives.

To learn more about securing your children’s financial future, consult a qualified financial advisor today. They can provide personalized guidance and help you develop a comprehensive plan that aligns with your family’s needs and goals.